Are you at that point in your life where you’re thinking about buying your first home?

You might have already done a bit of research about home prices. You might also have asked your mortgage broker how much you can borrow.

If you’re like most first home buyers, the chances are that the home you want in the area you like might cost around $450,000. Unfortunately, the banks have tightened their lending policies in recent times, so your mortgage broker might have told you that your borrowing capacity is limited to just $350,000.

So you’ve been told you can’t afford the home you really want in the area you like. What options do you have available now?

Rather than give up on your dream of buying your first home, take heart that there are still plenty of options still open to you.

Live in your first home or Rentvest?

Here are three options you might consider:

Option 1 – Rent in an area you like:

You might choose to think that the whole home ownership dream is too difficult and decide to stay renting in the area you really love. There’s absolutely nothing wrong with that strategy. After all, you get to live in an area you already like.

Just keep in mind that the house that might have been worth $450,000 today might have increased in value to $650,000 in 10 years’ time.

Option 2 – Buy in an affordable area:

You might decide to buy a more affordable home in an area nearby that is more in line with the amount of money your mortgage broker said you can borrow.

After all, it’s called your ‘first’ home because the majority of people eventually upgrade to a second family home as their family grows over time.

If you’re willing to start small and work towards paying down your mortgage balance as quickly as you can. If you’re able to build up your equity, you might be in a position to upgrade to a nicer family home in the area you really like in a few years’ time.

Option 3 – Rentvest:

If you’re like most people, options 1 and 2 are usually the first choices that come to mind. However, there is another alternative that many people overlook.

Rentvesting is the term used when you decide to keep paying rent in the area you really like, but you also choose to buy an investment property in an area that you can afford.

Perhaps the first question many first home buyers ask is ‘how can I afford a rental property if I keep paying rent somewhere else?’ Basically, the banks all look closely at your current income when they work out how much you can borrow. If you are going to rent out the property you buy, they will add the rental income you earn to your salary. The result is that you can often borrow a bit more than you first thought.

Advantages of Rentvesting

Rentvesting offers a few advantages that you might not have considered. Not only do you still get to live in the area you already love. But you are also buying an asset for the future that you can use to build your wealth.

Your tenants pay you rental income, which helps cover the cost of the mortgage payments and other costs associated with owning a home. Over a period of time, the value of the property should increase a bit. You also have the opportunity to start paying down the balance of your mortgage if you’re keen to build equity faster.

How capital growth helps – either way you go

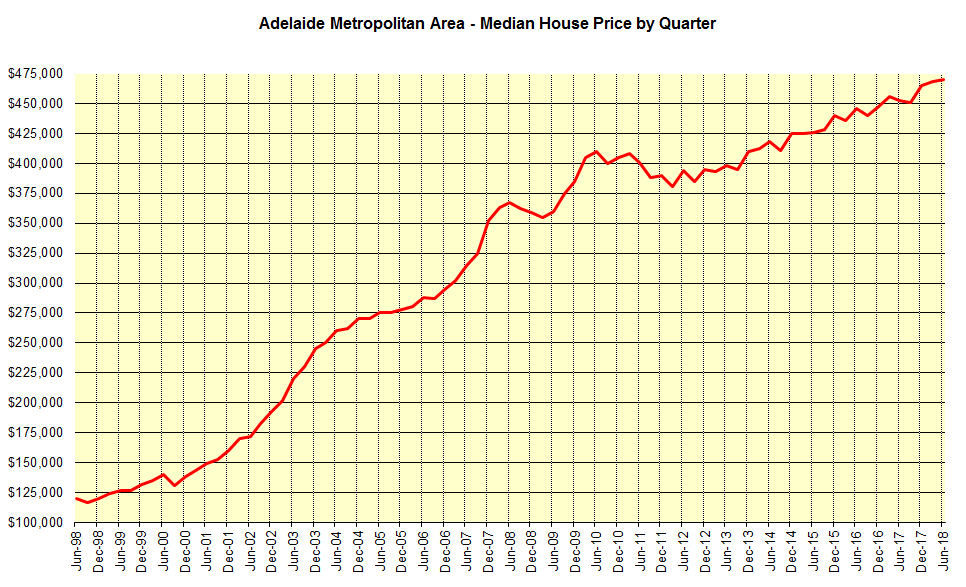

^ Adelaide house prices have risen $71,750 in the 5 years between June 2013 and June 2018.

If the housing prices follow the rule of 72, then if we divide 72 by 1 (at 1% housing market growth) it will take 72 years to double our money. However, if we divide 72 by 10% (10% market growth) it will take 7 years to double our money.

So in order for a property to double in value, you need a year on year growth of 7% for your asset to double every 10 years. Therefore 3.5% growth will mean a $450,000 house will be worth $675,000 in 10 years’ time.

What that means is if you invest into the market now, you have the potential to build $225,000 in equity on a growth rate of 3.5% over a ten year period.

As a landlord, your tenants are paying you rental income and you have the added benefit of increasing capital growth over time. Both options help to build your net wealth.

No matter what option you choose, the key to making the right decision for your financial future is to think carefully about what you hope to achieve. Take the time to speak to a good mortgage broker and discuss your choices with your accountant.

When you’re sure how each option might affect your finances, you’re in a much stronger position to make a choice that is right for your needs.